How to stay alert and healthy when selling your business

How to stay alert and healthy when selling your business

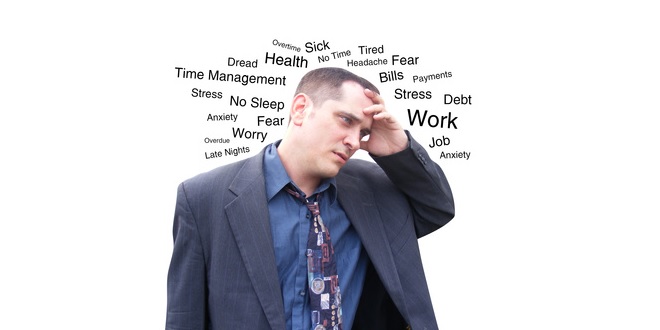

Selling a business is a tiresome and stressful process regardless as to the reason for sale. Whether it’s a distressed sale – selling due to health or personal reasons, or if it’s time to retire or move onto another adventure, the process can take it’s toll. And the ironic thing is that a business owner needs to fire on all pistons during the process. Not only does the owner need to prepare and jump through hoops to make the sale happen, but they also have to make sure the business performs! How to stay alert and healthy when selling your business is a massive factor on achieving success.

By now, we all know that stress sucks. From a scientific point of view, stress stimulates your body to secrete more adrenaline. Once it enters your bloodstream, adrenaline increases your breathing rate and blood pressure. Inevitably a person experiences physical weaknesses. With prolonged stress the body breaks down and eventually becomes ill or worse, gets diseased.

Stress is a consequence of a slight alteration in the natural state of the body. So any technique to reduce stress is to help bring your body back to its normal functioning. Below are some ways that can help you to counter stress:

Sunny side up

Look on the positive side of things. The glass is always half full and half empty – it depends on which version you want to focus on. You have the choice to focus on either. Keep in mind that there are millions and probably billions that have it far worse than you do. Count your blessings and remind yourself of all the great stuff you have in your life. Gratitude is a massive stress-buster.

Rest your way out

Some people fight stress by working towards resolving it. The ancestry of stress is usually over exertion so this in turn increases your brain-strain. Experts argue that taking a nap or simply resting while on a stressful routine can ease you out. While sleeping, the lobe of your brain responsible for voluntary thinking relaxes, hence it relaxes you. When I exited my company, I took up the practice of meditation. I couldn’t just sit in dark room for a 1/2 hour focusing on nothing, so I opted for ‘guided meditations’. Guided meditations often have nice music and someone talking you through a relaxation. You can download these over the Internet – they have mediation for everything. Stress reduction, enjoying life more, business success and so forth. Taking a 1/2 to focus your mind in a positive direction can work wonders.

Take a break

Remember to add short breaks to your fore-planned schedule. Go out for a jog or follow an influential personality on twitter regularly. Grab a book of your favourite author or start taking special interest in gardening. These activities will clear your mind out. Cycling, swimming and taking a brisk walk are effective stress relief exercises. Yoga is known for restoring the natural spiritual and physical state of the body. It might feel counter intuitive to take a break when you have mountains of work to do, however it will help to keep you sane. What’s more important? Your health or your work load? And strangely, you might discover that the more regular you are with your breaks, the easier and more productive your workload becomes.

You are what you eat

Take a healthy diet throughout the day. Water should be an essential component of your diet as it acts as a stress relief agent. Curb the consumption of alcohol and caffeine. (On this point, I have to admit, I couldn’t do that! I would have never survived without my 7am Latte and 6pm glass of wine!) I did however, eat salads, as much non-processed foods as possible and opted for healthier choices when I went out to eat. Think of it this way – you’re body is already stressed…don’t give it more problems to deal with.

A shoulder to cry on

Articulate your feelings instead of hiding or bottling them up. Find a good friend, mentor or family member to talk to. By exchanging comments and suggestions, you will gain exposure to a variety of ideas. Try your best to surround yourself with jolly people who live life optimistically. And stay away from people who make you unhappy and spread negativity as it can further strain your already stressed out brain. Develop a sense of humour and laugh for no reason at all – never loose an opportunity to smile. There’s a form of laughter healing – I can’t remember what it’s called but on certain days at a certain time a bunch of people all join a teleconference call and laugh. (Yes – this happens in the UK believe it or not)!

Give nature a shot

Once in a while, take a small trip to a place with a lot of natural vegetation and less noise. Take a walk and breathe in the natural scenery. Take a nap under the open skies and feel the nature around you. Once you get back to your daily routine after breaking its monotony, you will certainly feel lighter. Every time I go for a walk in the woods I often thing, ‘why don’t I do this more often!’ Just surrounding yourself in nature has a calming effect.

Last resort

Selling a business is an exasperating process. Running a business while trying to get the fairest sale deal can make anyone anxious. Stress builds up in your mind and body and leads you to experience physical deficiencies. If it gets to be too much seek professional help! There’s nothing and no one more important than you. If you go down so do the people around you so remember to put your health above all else!

Kim Brown, Co-Founder of Business Wand, helps business owners navigate their way through the start to finish process of selling a business. Her specialty is to help owners cut costs and increase profits prior to sale. To understand how you can sell your business quickly for the highest sales price, purchase the book, “How To Sell A Business: The #1 guide to maximising your company value and achieving a quick business sale”

Who better than to learn from one of the Sell Your Business co-owners, than Joanna! She can rightfully offer lessons learned from selling a UK business! I interviewed Joanna in the hopes that her experience will shed some light on various factors that might be able to help you or prevent you from making mistakes.

Who better than to learn from one of the Sell Your Business co-owners, than Joanna! She can rightfully offer lessons learned from selling a UK business! I interviewed Joanna in the hopes that her experience will shed some light on various factors that might be able to help you or prevent you from making mistakes.

Visualise your bountiful business exit, it’s worth it. Einstein considered imagination to be more important than intellect. Before doing an actual experiment, he would visualise the experiment in his mind, thinking about each and every detail and the whole sequence. As a result, he was prepared for the minor or major problems that he could encounter during the experiment. Establishing your business takes a lot of effort. It is only fair for you to consider a bountiful exit when selling your running business. However, like everything else, a business sale also requires a proper strategy. If you are well prepared, your business sale will conclude smoothly, with maximum returns for your hard work. The best way to be prepared for a business sale is to visualise successful business exit.

Visualise your bountiful business exit, it’s worth it. Einstein considered imagination to be more important than intellect. Before doing an actual experiment, he would visualise the experiment in his mind, thinking about each and every detail and the whole sequence. As a result, he was prepared for the minor or major problems that he could encounter during the experiment. Establishing your business takes a lot of effort. It is only fair for you to consider a bountiful exit when selling your running business. However, like everything else, a business sale also requires a proper strategy. If you are well prepared, your business sale will conclude smoothly, with maximum returns for your hard work. The best way to be prepared for a business sale is to visualise successful business exit.

Starting a new business all over again? What about your existing business? There can be many reasons for selling a business. It may be that you have realised that you are in the wrong line of business, and would like to switch industries. Or, you might have realised that your business is not performing as expected, and you would rather sell your business while it’s still making some profits. After all, over 50% of business start ups go under in the first five years. And, if you are lucky, you have a business that’s roaringly successful, and you would like to cash in the good will and start up a new business.

Starting a new business all over again? What about your existing business? There can be many reasons for selling a business. It may be that you have realised that you are in the wrong line of business, and would like to switch industries. Or, you might have realised that your business is not performing as expected, and you would rather sell your business while it’s still making some profits. After all, over 50% of business start ups go under in the first five years. And, if you are lucky, you have a business that’s roaringly successful, and you would like to cash in the good will and start up a new business.